Insuring the Future of the Insurance Industry

Chandan Chatterjee, Principal Consultant for Financial Services, writes on how today’s exceptional situation calls for fresh perspectives and creative solutions on the part of the Insurance Industry.

REAL IMPACT OF GLOBALIZATION

The proponents of globalization, back in the days, told stories about how globalization had the power to trigger economic development across the world, and how economic prosperity in one country had the power to trigger economic development in another. The world stood in awe witnessing success stories, however, the proponents seldom warned about the downside of this economic connectedness, that when one economy falls it triggers a landslide.

We have come too far for any discussions to change the way the world operates. We are all in the same sea and our fate depends on how we get hit by the next wave of the Covid-19 pandemic. It is a no-brainer to say that the world economy is on the brink of a glorious collapse and the collective might and intelligence of the world could not stop it from hitting us.

The impact of this pandemic is being felt across the world and industries. And for once, the impact on the insurance industry will be unprecedented. Back in 2013, a pool of insurance executives had revealed that a global pandemic was the single biggest risk that insurance companies had to prepare for. The moment of truth ominously arrived wearing the cloak of Covid-19. “For an average middle-class family today, the threat of shooting medical expenses is very immediate and real,” says LC Singh, Executive Vice Chairman at Nihilent. The situation can’t be any different for businesses, be it from any sector.

What makes insurance different is that in its role, it is expected to play in times of economic hardships, by helping companies and households manage risk and provide a cushion against losses. However, given the order of this crisis, insurers will most certainly find it difficult to safeguard their interest.

A BIG BLOW TO INSURANCE SALES

Furthermore, global businesses are failing. Businesses like aviation, hospitality, and tourism are at the forefront of the impact. With people cutting down on non-essential spending, many other businesses, like automobiles real estate electronics, etc, will come to bear the brunt of this downslide.

These industries contribute significantly to the sales of insurance products. But with these businesses is going out of the reckoning, the impact will be faced as severely by the insurance industry. The top-line numbers across insurance companies have taken a huge hit in India and globally.

Add to that, there is claim payment which has a direct impact on the bottom line. An interesting article by Sarah Kocianski on the impact of coronavirus on the insurance industry points out that paying out on policies will be a huge hit to insurance, and for reinsurers when added to their other exposure. This could put them in serious jeopardy. Imagine the plight of insurance and reinsurers, in them being out on cancellation of global events like the Olympics, exponential rise in healthcare claims, travel insurance claims, marine claims, property claims, etc. Suddenly, the pandemic starts to look incredibly serious for the insurance industry. And if that is not enough, the free fall of the market will be the final blow to their already battered spirits.

“Thankfully, we have all the basic building blocks in place says Yogesh Singh, who headed the Blockchain Practice at Nihilent until very recently. Taking the case of fraud, specifically around no-claim bonus, Yogesh explains how he rallied the industry titans to form a consortium. We leveraged the concept of distributed ledger to establish and maintain trust between parties, who otherwise wouldn’t have trust each other with claims information,” says Yogesh. He excitedly adds ‘look at the big results the solution delivered and tell me who would want to give it a miss’. In his new role of shepherding industry alliances, Yogesh has now engaged the regulator and remains buoyant about prospects for his product.

Insurance companies are having to respond on multiple fronts, as claims payers, employers, and as a fund manager. While each front has its challenges, the primary focus will be the well-being of its employees and the company’s ability to remain responsive to its customers.

It continues to be an industry where the call center number keeps buzzing through the day, the email servicing team finds itself dealing with the new batch of service requests and queries on every refresh, and sales personnel walking into its branches to ‘log in’ their new business applications. Being responsive across channels during such times can be both daunting and difficult. Due to a shortage of employees across servicing channels, all known performance metrics and service levels have started to look down the rabbit hole. Insurance is a serious business, given that it is put to use only on the occurrence of an unfortunate event, so being responsive is vital. Due to this, most insurance companies will tend to be more cautious and sympathetic towards the claimant. One tragic incident is enough to change public opinion. In the face of all the crisis that it has been dealt with, the insurance industry has shown tremendous resilience in the way it has reached out to customers and business owners to support them.

THE ROAD TO RECOVERY

Industry observer Chris Tidball in his commentary on the industry notes, “Covid-19 makes it difficult to predict what insurance can expect from the future. But we can look back at other crises and gain some meaningful insights into how claims organizations may be affected.”

When the curve flattens, and life begins to return to normalcy, we will potentially see more interesting claims dynamic emerge that will impact results into the foreseeable future. But it is too premature to predict the new world order for the industry. Yet, we know all industry champions and thought leaders are experimenting with ideas that will find a useful purpose in the days to come.

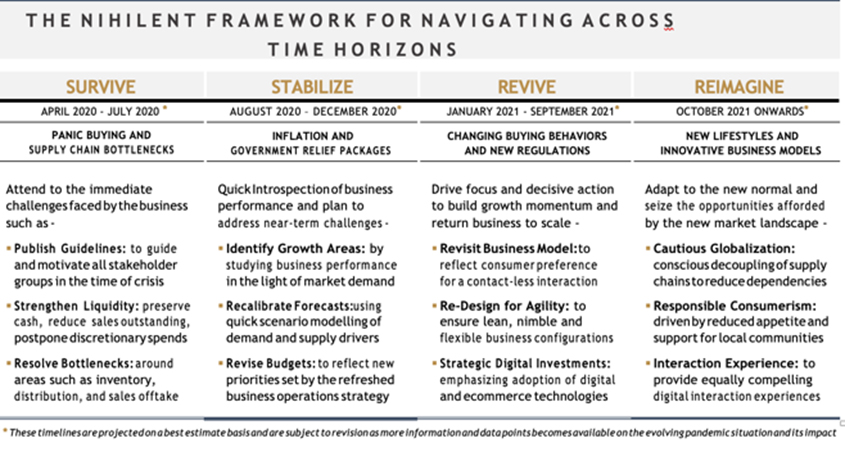

We present 4 distinct horizons along with specific focus areas for businesses to consider and prepare themselves for the long winding road to recovery. The first horizon, ‘Survive’ is about managing the turbulence, and seeks to address the immediate challenges that Covid-19 represents to businesses, their customers, workforce, technology, and business partners. The second horizon, ‘Stabilize’, seeks to assess recent business performance and address near-term challenges and the lockdowns economic knock-on effects. The third one, ‘Revive’ seeks to create a detailed plan to return the business to scale quickly as the Covid-19 situation evolves and its impact becomes clearer. The fourth wave, ‘Reimagine’ seeks to accelerate business growth by adapting to the new normal, by studying what a discontinuous shift looks like, seizing the opportunities through innovation.

Minoo Dastur, CEO at Nihilent, expects the insurance sector to make significant gains in the medium to long term. “The pandemic has rudely woken up the entire humanity to the importance of insuring their self-interests”, says Minoo.

However, this will not happen by default. Within this context, we outline a few priorities.

-

Risk assessment : We sense that the existing risk management models will go under the knife and re-purpose themselves to the changing times. The insurers will form their views on coverage for a claim based on specific policy language and the specific facts and circumstances of a loss.

-

Claims adjudication :Claims adjudication process will evolve from here. The current environment will see a lot of ‘ex- gratia’ payments, but all these transactions will be analyzed thoroughly and fed into the process to strengthen it, not to find faults and decline claims, but to ensure that necessary filters are applied to weed out fraudulent claims

-

Service enablement :The entire operating model associated with customer servicing will have to change. As work- from-home becomes an accepted practice for service delivery, the entire servicing value chain will have to be re-looked at and supported through the use of relevant digital tools and technologies. Back office processes like inbound and outbound call centers management will have to be reimagined. The existing ratios for capacity planning and workflow optimization have been rendered useless and if insurance companies need to remain responsible, they will have to take a hard look at its delivery mechanisms.

-

Industry-level initiatives to fight fraud : Fraud is rampant in insurance. Despite the rapid adoption of technology, the industry continues to be hit hard by fraud. In the days to come, we might see industry-level initiatives to fight fraud. A collective front will allow strong measures to be taken and apply universally. Universal application and adoption of fraud prevention practices will have a significant impact on the profitability of the industry.

The toll on the insurance industry is heavy and guess that is how lessons are learned. No one can predict when the next global pandemic will hit us, but it is evident that from now on, most businesses will be better prepared to realign themselves. The more we sweat in peace, the less we bleed in war.

An economist by interest, Chandan is an avid observer of financial regulations and government policies, and their impact on economic health of nations. He consults for financial services companies and remains particularly buoyant on fintech and its ability to accelerate growth that is affordable, inclusive and transformative.