Plotting a Quick Revival for Retail and Corporate Banks

Chandan Chatterjee, Principal Consultant for Financial Services, writes on how today’s exceptional situation calls for fresh perspectives and creative solutions on the part of the Banking and Financial Services Industry.

TAKING A MACRO PERSPECTIVE

The impact of the Coronavirus outbreak on humanity and businesses have been profound. As humanity continues to suffer, economies have come to a screeching halt. For governments across the world, it is an on-going conundrum of finding the right balance between getting their economy up and running without triggering multiple waves of this deadly pandemic.

While the impact of the Coronavirus outbreak on banking was not immediate, yet it was enough to send shockwaves. They have been good samaritans during this global crisis and have done everything in their means to provide their services as effectively as possible under the circumstances. People will remember this effort, although for a short period. Because in the coming quarters, the narrative will change. Banks will be under the radar and will be questioned about their de-risking measures and asset quality. Yet, it will continue to have a social obligation to support an economic turnaround of the economies.

DEEP IMPACT ON ECONOMIC ACTIVITIES

Given the unprecedented humanitarian and economic fallouts from the pandemic, banks have already started to review their exposure, and soon enough we will see a series of steps being taken to de-risk themselves. Moody’s points out, “A sharp decline in economic activity and a rise in unemployment will lead to a deterioration of household and corporate finances, which in turn will result in increase in delinquencies.” Therefore, the next 4 to 6 quarters will be crucial for banks as they re-align their business and move forward amidst strong headwinds.

The next few quarters will be testing time for the banks, especially, in developing economies. Acknowledging the challenges, LC Singh, Founder and Vice Chairman at Nihilent, encourages banks to take a conservative approach. He says, “We should not be overly simplistic, for the arc of disaster is going to be long. While banks will improve on their liquidity position, he believes that lending will not pick up steam due to demand destruction in the short-term as well as some supply-side challenges. Banks are expected to tread carefully and will take extra measures to not take on additional risks on their already weighed down portfolio.”

From a retail banking perspective, most banks will see their time and demand deposit balances growing manifold. Cut in discretionary spending, reducing appetite for market risk and a major shift in precautionary savings will result in a surge in balances held with banks.

Depending upon how close markets are to opening up, we foresee that this trend will continue for the next few months and banks will see margin pressures. The trend, however, may see a reversal the moment economic activity picks up and there is general traction in business operations. On the asset side, new business numbers will remain weak as the propensity to ‘borrow to spend’ will diminish.

However, the demand for secured lending will pick up once the market opens in the respective geographies. We may not see a huge surge in applications, but we will see moderate demand as people with a regular source of income may want to take advantage of the market conditions and buy assets at a beaten-down price with a lower cost of funds. Commission income from transactions like credit cards and debit cards will continue to remain weak amidst the lockdown measures implemented across the world.

“An interesting solution has been in the works for the last few months” says N Sundaresan, Vice President at Nihilent. The traditional ways of dealing with risk prediction have utilized data but leverage conventional techniques that give a discovery of the specific entity only, not the interlinked risk scenarios. This was quite helpful in some cases but fails to provide a true representation of the risk scenario that a bank or a financial institution was exposed to when dealing with financial instruments across varying levels of complexities in terms of construct, reach, scale as well as interactions including a variety of associated entities, financial institutions, locally as well as globally. The Affinity Risk Modelling solution from Nihilent seeks to leverage broader data sets to conduct thorough due diligence and create affinity-based red flags and the proportional risk intensity each of the affinity poses. In times like these, Sundaresan believes that this solution should be in every bank’s credit scoring toolkit.”

Banking companies will see severe earning pressure in the MSME (Micro, Small, and Medium Enterprises) segment. In developing economies, MSMEs play a huge role in keeping the economy buzzing and acts as the engine for economic growth. They contribute anywhere between 25% – 52% of the GDP of developing economies and their well-being is key to ensuring the revival of any economy. On top of that, they generate substantial employment in the metro, urban, and semi-urban areas. Due to the lockdown, most of these entities are staring at a dismal future. Their order books are running dry and so is their ability to keep paying wages. Therefore, anybody guesses that a vast number of these units will be choked, possibly to the point of imminent closure. And these are unprecedented times, even borrowers with unblemished track record could encounter cash flow issues because of cascading effects of disruptions and dislocations in this intertwined world.

“This won’t be like the great depression,” says Minoo Dastur, CEO at Nihilent. “When the global economy went backwards for four consecutive years”. Minoo however quickly points out that time will be of the essence and adds that the onus of creating a conducive environment for quick recovery lie squarely with the governments of the day. Few governments have indeed woken up to protect their economic interests and most countries have introduced stimulus packages in the form of the extra credit line, an extension of moratorium periods, eased access to working capital financing, deferred interest without downgrading asset classification and credit guarantees. While these interventions allow some breathing space for the MSMEs, their problems are far from over for both, MSMEs and the banks. Banks, as we are given to understand, are constantly monitoring their MSME portfolio and reviewing every single relationship.

The objective may not be to reduce exposure from a risk angle but to divert liquidity where the need is more pressing. Further, we will see some re-alignment in the portfolio and banks will steer towards secured lending to avoid any increase in credit costs. In the MSME segment, for banks, it is a tug-of-war between economic prudence and business relationships. We will have to wait for the situation to play out to ascertain the exact nature and depth of impact.

From a corporate banking perspective, we think that it is best to judge every relationship based on its industry. We see tremendous stress coming in from companies that are into hospitality, retail, travel, aviation, real estate, electronics, and automakers to name a few. And, impact on these industries will lead to a cascading effect in industries like cement, oil and gas, OEMs, iron, and steel, etc. While some of these industries are cash-rich and can sustain for a longer period, we largely believe that banks will enter a new cycle of bad loans. Banks all over are being inundated with requests for credit. These requests will keep increasing in the coming weeks as cash reserves run dry. Therefore, near term bank decisions will have a huge impact on the economic consequence. Due to credit defaults, we see the risk-weighted assets of the bank increasing as a percentage of the total assets which may get the banks ready to raise capital in a year or two.

“Sooner or later, agonizing trade- offs between saving lives and saving livelihoods will have to be made,” says Minoo Dastur. Leaders will be pushed to make difficult decisions that trade-off between protecting the balance sheet of the bank vis-à- vis what will spur companies and communities to revive.”

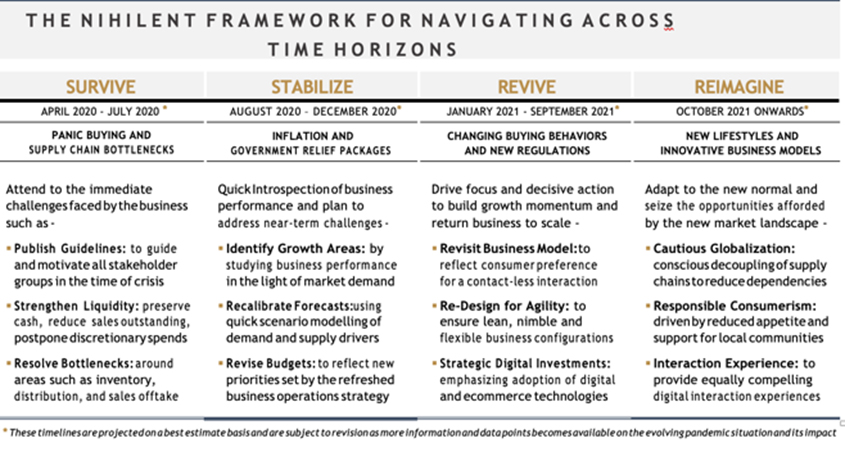

CONVERGENCE OF ACTION WILL BE THE KEY

We present 4 distinct horizons along with specific focus areas for businesses to consider and prepare themselves for the long winding road to recovery. The first horizon, ‘Survive’ is about managing the turbulence, and seeks to address the immediate challenges that COVID- 19 represented to businesses, their customers, workforce, technology, and business partners.

The second horizon, ‘Stabilize’, seeks to assess recent business performance and address near-term challenges and the lockdowns economic knock-on effects. The third one, ‘Revive’ seeks to create a detailed plan to return the business to scale quickly as the COVID-19 situation evolves and its impact becomes clearer. The fourth wave, ‘Reimagine’ seeks to accelerate business growth by adapting to the new normal, by studying what a discontinuous shift looks like, seizing the opportunities through innovation.

The jury is perhaps still out on the exact response from the banking sector. Depending upon the impact of the pandemic, banking sectors across the world will take decisions that will be relevant to the markets they serve.

Thematically though, we see some broad-based areas of convergence of action, and we outline them below:

-

Assessment of existing portfolio: All banks have already started taking a hard look at their portfolio. A joint task force of sorts comprising of members from the product, sales, and credit team would review every sector and try to assess the stress. This will help shape the near-term lending strategy and capacity.

-

Drive responsiveness: All service metrics had nose-dived due to the lockdown. Banks, being part of essential services, is a public-facing industry that needs to keep its doors open. They are exploring ways to ensure that service delivery is up and running without putting the employees in harm’s way. Options like the primary site, secondary site, and tertiary sites are being explored to ensure employees can slowly get back to work in alignment with safety measures laid out by respective health agencies/ministries.

-

Re-aligning credit decisioning framework:It is uncertain at this point if credit models and frameworks will change forever but a course correction is imminent in the near-term. Banks will have to take some very tough decisions on their credit decisioning framework keeping in mind the need to protect capital and yet, deploy excess liquidity to generate economic momentum.

-

Advising clients on resource handling and restructuring: We foresee a lot of banks working closely with their clients as partners in their revival process. If we take a deeper look at the MSME segment, it is not difficult to understand why. Most MSME companies lack financial management knowledge, and therefore, discipline. Many lack a dedicated finance team/unit that can run forecasts, cashflow projects, etc. The ability and willingness in banks to aid them will not only instilling the right discipline but will also provide a detailed view of the need and application of capital in this segment.

When all business performance parameters are heading south and the economic macros are still in a state of flux, charting out a clear path is difficult. We believe that, like most organizations, banks will define 90-120-180-day plans to navigate this evolving global crisis. To predict the future with a sense of accuracy, when the crisis is still ongoing, seems unwise. We will have to wait for another quarter or so to pass by to get a sense of what lies ahead. But we are certain that the pandemic will bring both challenges and opportunities in the medium to long-term.

An economist by interest, Chandan is an avid observer of financial regulations and government policies, and their impact on economic health of nations. He consults for financial services companies and remains particularly buoyant on fintech and its ability to accelerate growth that is affordable, inclusive and transformative.